Hello once again! I am so sorry for the brief hiatus. Things get so busy from time to time and I am terrible at putting activities into daily slots. However, I am committed to this endeavor and will have to dedicate time to writing in order to make sure that I am bringing relevant and interesting content to you on a regular basis. My goal is to get out a minimum of two posts per week. I hope to get on this regular scheduling starting next week. Thanks so much for your understanding.

Now on to today’s topic ….. How do you pick stocks?

Memorable Quotes About Stocks

- “If you’re emotional about investing, you’re not going to do well. You may have all these feelings about the stock, but the stock has no feelings about you.” (Warren Buffet in the HBO documentary Becoming Warren Buffett)

- “Don’t get emotional about a stock. It clouds your judgment.” (Michael Douglas as Gordon Gekko in the 1987 film, Wall Street)

- “Buy the dips. Sell the rips.” (Quote is taken from The Wall Street Daily News, 1988)

- “I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.” – Warren Buffett

- “The individual investor should act consistently as an investor and not as a speculator.” – Ben Graham

- “Know what you own, and know why you own it.” – Peter Lynch

- “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” – Paul Samuelson

- “The stock market is filled with individuals who know the price of everything, but the value of nothing.” – Phillip Fisher

- “The only way one should buy stocks is if you understand the underlying business. You stay within the circle of competence. You buy businesses you understand.” – Mohnish Pabrai

- “How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case.” – Robert G. Allen

These quotes say a lot more about investing in stocks than most of what this post will, but if you can humor me for a few moments, I will add more color to some of these timeless quotes on the art of stock picking.

Are you an investor, trader or speculator?

So, the first question I will typically ask a client is whether they are an investor, trader or speculator.

Note – Before I dive into this, please be aware that I am “going light” on this topic. I am not going to get into Top-Down Analysis, Bottom-Up Analysis, Charting, or hard core fundamental analysis (e.g., Discounted Cash Flow Analysis), etc. At least not yet. So bear with me as I break it down for common folks without MBAs in Finance (smile).

So, what’s an investor? To keep things simple, we will define investors as individuals that are interested in buying stable, well-run companies and do not have a defined date for selling the stock (as long as the company continues to run well and its stock price is relatively stable). So hypothetically, these can be purchases that can be made, and the stock held indefinitely. This post is mainly for investors.

Traders are individuals that buy in and out of stocks. They can hold stocks for months, weeks, days, hours, minutes, and even seconds! Traders look for large swings in the price of a stock to make profits. Another distinction for traders is that they don’t necessarily buy a stock with the hope that the stock will go up in value. Short sellers or put option buyers trade with the hope that a stock will decline in value. “Short” activity on a stock can sometimes act as a leading indicator as to whether a stock will change in value – not necessarily due to fundamental flaws in the stock’s business, but due to market/trading forces (i.e., a stock can go up in value simply because short sellers have to “cover” their shorts by buying shares). I will get into puts and shorts on another post, but just understand that traders typically take short-term positions on a stock that can be based on a positive (hope that the stock will go up) or a negative (hope that the stock will go down) bias. This post is not for traders, so if you’re looking to trade stocks, this post isn’t for you.

Speculators are simply people who buy heavily depreciated stocks or short highly priced stocks in hopes of making a profit. They take positions that can be either short-term or long-term in nature. Again, this is a post for investors, so I am not going to get into speculation at this time.

Identifying Stocks for Investors

Here are some thoughts/ideas and pointers for identifying stocks that might appeal to you as an investor:

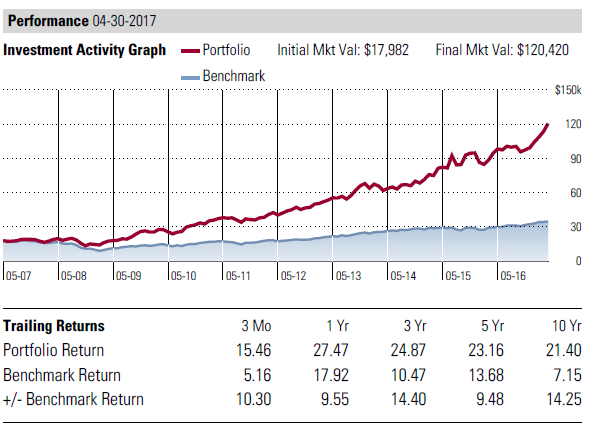

- Buy What You Know – This past November, my daughter (who was 8 at the time) picked five stocks for a school project. She picked the following stocks – (1) Disney because she loves watching the Disney Channel (DIS), (2) Amazon (AMZN) because we order everything from the site, (3) Panera (PNRA; going private) because she loves going there for lunch and snacks, (4) BlackRock (BLK) because I used to work there (smile) and (5) Novartis (NVS) because they make Triamedic cough medicine which she takes at home, and she postulated that with winter coming up “people were bound to get sick and need medicine.” This is the performance of the stocks between November 2016 and April 2017:

You read it right, she made more than 15% in three months. That’s over $1,500 made on a $10,000 investment made in 90 days. Compare that to the less than 1% that you can get from a checking account, or 1.85% for an 18-month CD. Look at companies behind the goods and services you buy every day. Go online and do some research. Are these companies profitable? Do their profits and/or performance have a track record of going up consistently? Are they among the top 5 participants in their respective industries? Is the stock price steady growing? Does the stock pay nice dividends? If there are enough “yes” answers to these questions, you may have a stock that you can invest in.

- Understand the businesses behind the stocks you buy – I can’t impress on you to get a strong understanding of the businesses that you invest in. Fortunately, you don’t have to be a wall street analyst to do research on the internet. In fact, most of these companies provide you the information that you need by looking at their own financial statements (found on the company’s own website or www.sec.gov ). User-friendly websites like Google Finance, Yahoo Finance, CNBC, Bloomberg, etc. all have tons of data and summarized information at your fingertips. For every company, you want to know the company’s (1) Strengths (industry leader, solid historical stock performance), (2) Weaknesses (weak customer service, sub par product, technological obsolescence, etc.), (3) Opportunities (potential merger, new product development), (4) Threats (rising competitors, technological threats, unfavourable governmental legislation, etc.). Buy investments in ignorance at your own peril.

- Don’t confuse speculation for analysis – I can’t tell you how many clients, friends, family, and acquaintances approach me with investment ideas based on speculation vs. actual knowledge of a company’s market or actual opportunities. “I believe that the company is going to do this” or “If this technology catches on, the stock could fly”, are things I often hear. It sounds great, but when I ask for evidence – numbers, research and how projected growth translates into a higher stock price – I get “Ums” and/or “Wells”. How about when such ideas fail or never come to fruition? Do these prospectors (because they are certainly not investors) have an exit plan? If so, at what price do you sell? What will be the trigger to sell? As you see, it isn’t hard to undress a speculator masquerading as an investor. If you want to speculate, go to the casino. The stock market is not a place to be placing half-cocked bets. There’s nothing wrong with taking insignificant chances on a name or two once in a while, but understand that you should be making such bets with money that you’re comfortable losing. If not, don’t do it.

Conclusion (for now)

There is no foolproof way for picking winning stocks, so understand that it is likely that when investing in individual stocks you will pick winners and losers. If you have the stomach to get through it and learn from the experience, I do encourage you to embrace this wealth building activity. Lastly, you should consider building the foundation of your portfolio with broad-based market exposure via a low-priced stock market index fund or ETF. Then you can look to invest in single name stocks to help enhance growth opportunities.

I hope that you found this post informative and helpful. As always, I am available if you have questions to discuss. In the meantime, good luck!