Do you participate in your employer’s flexible spending plan? If not, you may be leaving hundreds to over $1,000 in tax savings on the table.

I thought about flexible spending accounts (FSA) today when I dropped my daughter off at camp. She goes to a moderately priced summer day camp that charges around $400 a week, and that’s cheap for Central NJ. Ok, so let’s do the math. $400 for camp plus $50 for lunch times 10 weeks equals $4,500! I thought to myself that these prices are obscene, and thank goodness that I funded an FSA with the pre-tax funds to pay for it!

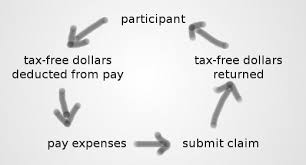

So, what is a Flexible Spending Account, or FSA? An FSA is an employer-sponsored benefit that is offered to employees. The employee is offered the opportunity to fund an account on a pre-tax basis to cover out-of-pocket costs up to $5,000. There are two types of FSAs – one for out-of-pocket medical care costs (a “medical care FSA”) and another for dependent care costs (a “dependent care FSA”). For most employees, you have the ability to contribute up to $5,000 in both (there are employment benefit rules that may limit the amount that an employee can contribute to the dependent care FSA; however, you can always contribute the maximum to a health care FSA). This maximum applies on a per household basis. So, the maximum that can be contributed is $10,000 per household ($5,000 for dependent care FSAs and $5,000 for medical care FSAs).

Benefits of FSAs

- You save on taxes – Depending on your tax bracket, you stand to save a significant amount of taxes on out-of-pocket medical care expenses and/or dependent care expenditures. In addition, not only do you save on income taxes, you also save on federal payroll taxes (1.45 % Medicare and 6.2% Social Security taxes). For example, consider a family that earns $150,000 annually, has a 3-year-old in day care (annual cost of $13,000) and $2,500 in out of pocket medical care expenses (health insurance co-pays, eye-exams, and new glasses, etc.), and is in the 28% tax bracket. With a family contribution of $7,500 ($5,000 maximum for dependent care and $2,500 for medical care costs), the family will save $2,673.75 in taxes. That’s cash in your pocket and not in Uncle Sam’s! That’s you and your wife’s life insurance premiums (assuming 30-yr term policies with good health ratings). That’s a vacation. That’s money to pay down consumer debt. That’s money to put towards savings, or to make an annual lump prepayment on a car note or student loans (if applicable). The point is, this is money that wasn’t there before.

- You’re using the funds on things you would pay for anyway – This should be a no-brainer, but for families with (a) dependents that are not old enough for kindergarten, (b) dependents under the age of 13 that need before- or aftercare, or attend day summer camp (sorry – sleepover camp doesn’t qualify), or (c) elderly dependents that attend daily elderly care, this tax benefit can come in handy.

- Technology makes it easy to access FSA funds. Many administrators provide debit cards to make it easy to pay for qualified services. Some even pay the service provider directly on your behalf. Online portals also make it easy to submit receipts for prompt repayment.

Downsides to FSAs

- Use it or Lose It – You have to be careful in projecting the future medical and dependent care expenses that you plan to spend in the upcoming year. Budget too little and you may lose the excess of your account balance. Here’s a quick example. The Jones family budgeted $2,000 in medical costs for the year but only spent $1,300 by December 31st of the current year. That leaves an excess of $700 in the account. In the past, the entire $700 would be forfeit. However, new regulations do allow you to rollover a maximum of $500 from the current year to the next or allow you up to March of the ensuing year to incur qualified expenses (and up to April to request reimbursement). Many plans differ in how they administer overages in an FSA account, so make sure that you do your research and budget carefully before designating an amount for the FSA plan.

Qualified Expenses

So what qualifies as a qualified healthcare and dependent care expenditure? Here are a few examples:

Medical Care Costs

- Out-of Pocket Co-Pays, Deductibles Co-Insurance Associated with Health Insurance

- Out-of-Pocket Deductibles associated with Dental or Eye Insurance

- Medical Transportation Costs (documented)

- Prescribed Medications (Over the Counter, even if prescribed do not qualify)

- Medical Supplies (with prescription)

- Urgent Care Center Expenditures

- Long-Term Care Insurance Premiums

- Eye Exams and Eyeglasses (prescription)

Dependent Care Costs

- Daycare (pre-kindergarten)

- Summer Camp (dependent under 13; Sleepover Camp does not qualify)

- Before- or After Care for dependents under 13

- Babysitter Costs (dependents under 13 and babysitter is not a dependent)

- Elderly Dependent Day Care (must be needed for both spouses to work)

Thanks for reading. Feel free to contact me with any questions!