Do you have a solid foundation upon which you can build wealth?

The other day, I received a call from a young 40-something client about retirement planning. “I have two little ones and my wife and I want to make sure that we are doing what we’re supposed to do in getting ready for retirement.” The client also expressed a desire to invest ~$6,000/yr towards college savings via 529 accounts ($250 per month, per child).

While this all sounded respectable and fair, I stopped him in his tracks and said “(Client), I am so happy that you’re being proactive in reaching out to me to discuss and address these issues, but I think we need to step back for a second. We need to look at the foundation upon which you’re looking to build.”

I could tell that my client was puzzled. He proceeded to ask me what I meant. I explained that as an advisor, I strive to develop plans with the strongest chance of succeeding. I am not interested in laying out colorful pages full of rosy assumptions, pretty graphs and a product push on the back-end. I am a professional that breaks down your goal as you communicated it to me, designs a plan to achieve that goal, identifies the risks that can throw a monkey-wrench in that plan, and finally presents solutions that eliminate or mitigate those aforementioned risks. “If we have a plan that ignores risk, we don’t have a plan. We have a pretty looking wish list.”

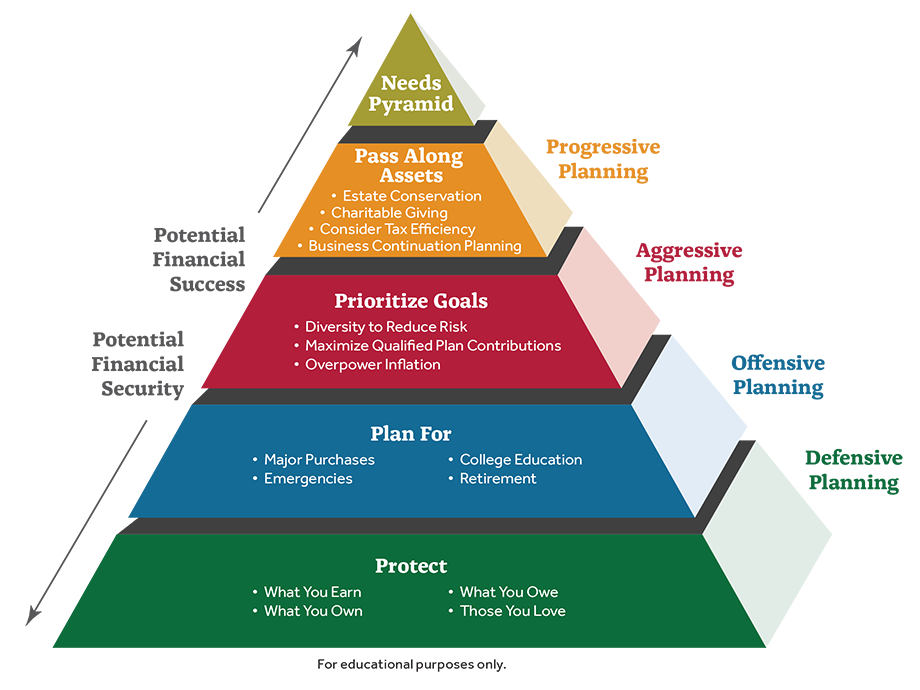

To develop this foundation of protection, I proceeded to describe to the client a foundation on a home. It has a simple, Pyramid-like shape with protection at the base. These are the four areas of your life that need protection – (1) health, (2) financial, (3) personal property and (4) wealth.

Health – To protect your health, you need health insurance and adequate reserves to handle extreme medical emergencies such as max out-of pocket deductibles and co-insurance. Having those funds in liquid cash, in a Health Savings Account are ways to manage this risk. Insurers like AFLAC also have special products to mitigate this risk for middle to low income earners that find it challenging to accumulate such funds.

Financial – Protecting your financial situation is a multi-faceted strategy. At the base of the plan, one should secure adequate Disability insurance. This coverage “protects the paycheck” and insures that you have the funds needed to meet financial obligations in the event that you can’t earn an income due to accident, illness or affliction. Next, would be adequate life insurance. Having a plan for your family is useless if you die and the resources needed to support surviving family is not there. Insurance is the best way to leverage relative lower dollars to generate a legacy for years to come. Building up an emergency fund and paring down debt are also methods of insuring that a savings/investment plan has a maximum chance of success.

Personal Property – Most of these items are required to be protected – auto insurance, homeowners’ insurance, apartment insurance, umbrella coverage, etc. it’s funny how the powers that be (banks, landlords, auto finance companies) make it required for you to protect their things, but we fail to require ourselves to protect our own valued assets.

Wealth – Strategies like proper asset allocations, utilization of protection-focused instruments like annuities and structured products are all ways to help minimize risks to retirement portfolios. In addition, forward-looking asset protecting vehicles like Long-Term Care help retires keep their assets from being decimated by custodial needs that may arise later in life.

While all of these issues may not be applicable to my client in the present sense, discussing these issues help clients see the big picture and plan accordingly. We identified (1) that his emergency fund only covered two months of expenses, (2) there were shortfalls in his life insurance and (3) that his long-term disability coverage didn’t cover his annual bonus (which made up nearly 40% of his annual compensation). So the plan right now was to secure the needed supplemental disability and life insurance immediately, cut back spending and build his emergency fund up to be a MINIMUM of three-month’s expenses (the 18-month goal is to build this up to 6 months of income), continue to responsibly manage debt, open two 529 with lower contributions (but reaching out to family and friends to contribute to help build up the account), and finally develop a risk- and time horizon-adjusted asset allocation analysis for the retirement portfolio. By engaging in actions to fortify his financial foundation, we are now both in a better position to work together to build wealth.