Here’s my first article for Personal Finance Insider, where I share information about the types of people who need insurance the most, in my humble opinion. Please read and share your opinions with me. Thanks!

See the Article Here.

Musings of A Professional Problem-Solver

Here’s my first article for Personal Finance Insider, where I share information about the types of people who need insurance the most, in my humble opinion. Please read and share your opinions with me. Thanks!

See the Article Here.

Do you have a solid foundation upon which you can build wealth?

The other day, I received a call from a young 40-something client about retirement planning. “I have two little ones and my wife and I want to make sure that we are doing what we’re supposed to do in getting ready for retirement.” The client also expressed a desire to invest ~$6,000/yr towards college savings via 529 accounts ($250 per month, per child).

While this all sounded respectable and fair, I stopped him in his tracks and said “(Client), I am so happy that you’re being proactive in reaching out to me to discuss and address these issues, but I think we need to step back for a second. We need to look at the foundation upon which you’re looking to build.”

I could tell that my client was puzzled. He proceeded to ask me what I meant. I explained that as an advisor, I strive to develop plans with the strongest chance of succeeding. I am not interested in laying out colorful pages full of rosy assumptions, pretty graphs and a product push on the back-end. I am a professional that breaks down your goal as you communicated it to me, designs a plan to achieve that goal, identifies the risks that can throw a monkey-wrench in that plan, and finally presents solutions that eliminate or mitigate those aforementioned risks. “If we have a plan that ignores risk, we don’t have a plan. We have a pretty looking wish list.”

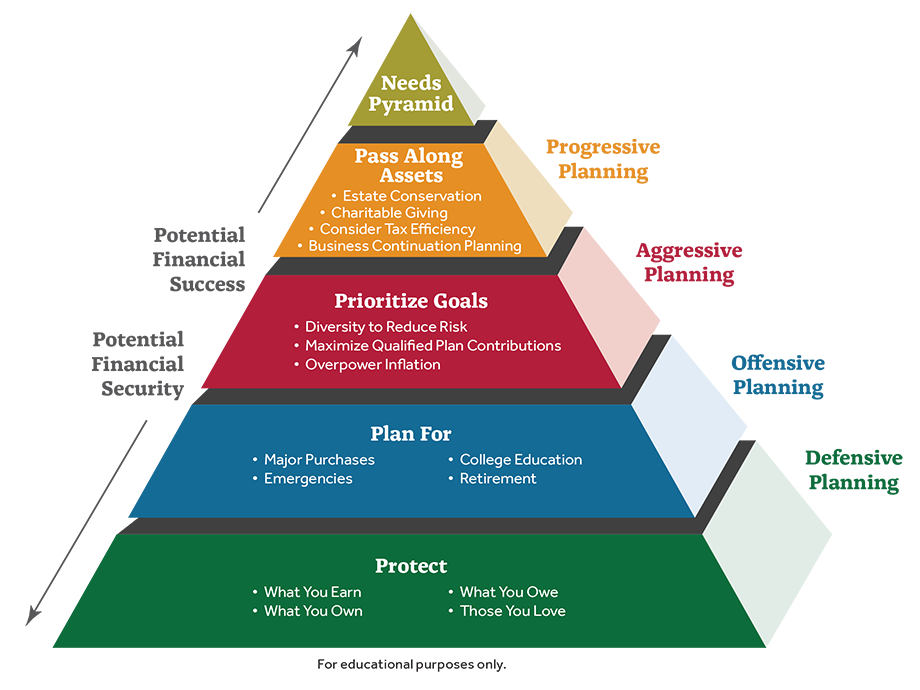

To develop this foundation of protection, I proceeded to describe to the client a foundation on a home. It has a simple, Pyramid-like shape with protection at the base. These are the four areas of your life that need protection – (1) health, (2) financial, (3) personal property and (4) wealth.

Health – To protect your health, you need health insurance and adequate reserves to handle extreme medical emergencies such as max out-of pocket deductibles and co-insurance. Having those funds in liquid cash, in a Health Savings Account are ways to manage this risk. Insurers like AFLAC also have special products to mitigate this risk for middle to low income earners that find it challenging to accumulate such funds.

Financial – Protecting your financial situation is a multi-faceted strategy. At the base of the plan, one should secure adequate Disability insurance. This coverage “protects the paycheck” and insures that you have the funds needed to meet financial obligations in the event that you can’t earn an income due to accident, illness or affliction. Next, would be adequate life insurance. Having a plan for your family is useless if you die and the resources needed to support surviving family is not there. Insurance is the best way to leverage relative lower dollars to generate a legacy for years to come. Building up an emergency fund and paring down debt are also methods of insuring that a savings/investment plan has a maximum chance of success.

Personal Property – Most of these items are required to be protected – auto insurance, homeowners’ insurance, apartment insurance, umbrella coverage, etc. it’s funny how the powers that be (banks, landlords, auto finance companies) make it required for you to protect their things, but we fail to require ourselves to protect our own valued assets.

Wealth – Strategies like proper asset allocations, utilization of protection-focused instruments like annuities and structured products are all ways to help minimize risks to retirement portfolios. In addition, forward-looking asset protecting vehicles like Long-Term Care help retires keep their assets from being decimated by custodial needs that may arise later in life.

While all of these issues may not be applicable to my client in the present sense, discussing these issues help clients see the big picture and plan accordingly. We identified (1) that his emergency fund only covered two months of expenses, (2) there were shortfalls in his life insurance and (3) that his long-term disability coverage didn’t cover his annual bonus (which made up nearly 40% of his annual compensation). So the plan right now was to secure the needed supplemental disability and life insurance immediately, cut back spending and build his emergency fund up to be a MINIMUM of three-month’s expenses (the 18-month goal is to build this up to 6 months of income), continue to responsibly manage debt, open two 529 with lower contributions (but reaching out to family and friends to contribute to help build up the account), and finally develop a risk- and time horizon-adjusted asset allocation analysis for the retirement portfolio. By engaging in actions to fortify his financial foundation, we are now both in a better position to work together to build wealth.

Now, Where Were We?

Hello there. Thanks so much for reading my blog. As this post is a continuation from last week’s post, if you haven’t had a chance to read it, please take a look at it here. I will now continue my “self-interview” on all things involving life insurance.

We get it. You are a big proponent of having insurance – either in the form of

Answering such a question is highly subjective. I mean, life insurance is such a personal purchase, and it is the most unselfish thing that you can buy for the people you love, that I often struggle with the question regarding “how much is enough” or “how much should I buy”. That is exactly why I engage clients in planning – so I can listen to them, understand their goals, get a sense of their value system, and try to serve as a guide and resource in helping them find the right balance of protection to meet their needs. Simply saying “7-10 times salary” doesn’t do the planning process any justice.

How much do you need?

So, in trying to answer this question I often do my best to ascertain answers to the following two financial questions: (1) how much is financially needed immediately upon your death and (2) for the foreseeable future, how much is financially needed to meet the shortfall in financial needs due to your death. Then you add (1) and (2) together and subtract the sum of: (3) existing life insurance, (4) social security benefits (if any), and (5) any assets that you currently have in place to meet the needs of (1) and/or (2).

Immediate Needs are financial needs/

Future needs are a little more complex and oftentimes requires a financial calculator of some sort, but I will try my best to be simple. In looking at future needs, I take the lost financial resources (salary, retirement savings, asset accumulation, etc.) and compare that to the resources needed under the new plan (one where a financial provider is gone, but there remains to be needed for household maintenance, child care, college planning, retirement planning, etc.). This often entails multi-stage analyses when dealing with young children (where Social Security can be contemplated), teens and college-age children, and the surviving spouse as a pre-retiree and retiree). Those needs are then computed into an amount needed now to fund the shortfall, which is the Future Needs component of life insurance.

Next, you add the Immediate and Future Needs to arrive at the Tentative Need. Finally, you subtract the combination of Social Security your surviving family is expected to receive, existing life insurance, and existing assets (in place for the purposes that the insurance is intended to be used for) from the Tentative Need to arrive at your Insurance Need. This is not the easiest stuff to come up with. Thank goodness that there are calculators on the web and trusted professionals out there that can assist you in the process.

In determining what amount should be term coverage vs. permanent coverage. It’s highly subjective, but I generally recommend that families use the “temporary need for

Lastly, this analysis is representative of how I derive insurance needs with a majority of clients that I service. It should be said and made clear that everyone’s situation is different. With that said, it is not my aim to tell you that the approach that I described is the best way that works for you and your family. There are many different situations – families with children who have disabilities/special needs, breadwinners with generous pensions, or a married couple with no children, but provide for parents/other loved ones, etc. The list goes on and on, but the point to drive home is that different facts, circumstances, makeup of net worth and makeup of existing coverages impact the calculation and derivation of the amount of insurance needed (if any) as well as the structuring of such coverage (i.e., the term life vs. permanent life, or combination of the two).

Stay Tuned. There’s more to come.

Please come back next week for the final part of this discussion on Life Insurance. I hope that the information shared is helpful to you and those that you love. As always, feel free to contact me via Facebook or Twitter to ask questions or discuss the topic in more detail. Thanks!

Hello everyone and Happy New Year!

Welcome back to my blog. On the date of this post, I am dealing with the one-year anniversary of my father’s death (February 5th), mired with a myriad of emotions and nostalgia. I had a complicated relationship with my father growing up, but as I became a father and have grown in that space, I have come to acknowledge and appreciate him more and more – even though he is no longer here.

Without getting into too much detail, my father died unexpectedly (he was in relatively normal health for a 75-year-old) and caught my family off-guard. Luckily, we were able to handle the financial impact and with only my mother and siblings as the surviving immediate family members, there was little to sort out by way of probate/estate. Yes, we were lucky.

Yes, lucky indeed. But what about families in different or more complex situations? How would they deal with the sudden or unexpected death of a loved one who is a significant financial provider to the household? The easy and almost textbook-like answer is “life insurance”. It is general and widely accepted knowledge that many low- and middle-class families look to financial products like life insurance to help families “pick up the pieces” in the aftermath of the death (whether unexpected or not) of a loved one, especially one that served as a main income provider to the household. However, such widely held knowledge and understanding does not translate into life insurance ownership. According to a 2017 Life Insurance Study conducted by LIMRA, the following statistics state the following – and it isn’t that positive.

The Study (or other information from LIMRA) cites the following statistics:

The Study also provides insight as to why current prospective consumers of life insurance currently do not own it:

So what does this all mean? When it comes to life insurance,

Now that I have done a quick rundown on the status of life insurance in the typical American household budget, I thought I would change up my typical “chat-style” blog format and discuss life insurance in the form of an interview transcript. In addition, as the title of this entry says, I plan to provide “the real” response on these issues, and not provide “agent-speak” (the type of jargon that you would expect to hear from a life insurance sales agent – and this is not to imply that an agent would tell you something improper).

How important is life insurance to a family’s financial plan?

I firmly believe, that next to disability insurance, life insurance ranks as the #1 financial priority of a household, as no other product has the financial capability of completing the financial plan (i.e., if you die, the death benefit is paid to fund college, retirement, pay bills, fund emergency reserves, etc.) if you were to die.

OK. We get that you’re passionate about life insurance. Many working Americans already have

I’ll let you in on a dirty little industry secret – If you’re healthy, privately sourced term life insurance is CHEAPER than the group coverage that you pay for through the job! In order for group coverage to be affordable across the board, the healthy subsidize the unhealthy. Therefore, group coverage charges healthy insurance premium payers more than they otherwise would pay so that the unhealthy can obtain comparable coverage at an affordable rate. So, if you’re unhealthy or have a health condition that would be really expensive to cover, group coverage is a great deal for you. If you’re in reasonable health, you can get a private policy that beats that group coverage price over the life of the policy (group policies typically raise rates over 5-year increments).

As far as considering if group coverage is enough? I would say no simply because (a) there’s a question whether the coverage that you’re buying is portable, or that the coverage can be converted into privately-owned coverage if you leave your employer, and (b) many group plans do not allow employees to secure 7x salary (so the need isn’t being fully addressed by group coverage). Take whatever life coverage that the employer gives you for free (1-2x salary), but if you’re going to pay for any additional life insurance, price it out in the private market first.

What about Additional Death and Dismemberment Insurance (AD&D insurance)? Do you recommend that consumers buy this coverage?

In a word, NO. Without getting into too much detail, AD&D insurance pays the insured if he/she dies or suffers a severe injury (i.e., loss of limb) as a result of an accident (not of their own doing). It costs a fraction of the cost of term coverage because you have to die or be severely injured by accident in order to be paid a benefit, which is an unlikely event. I don’t like managing risks (i.e., dying) with a product that only pays if you die under certain circumstances.

Let’s explore the Term Insurance vs. Permanent Insurance issue. Many “financial experts say that you should “buy term and invest the difference”. What are

I have so many thoughts on this issue, but let’s start with the basics.

First of all, term life insurance is just that – life insurance that lasts for a certain “term” (i.e., annual renewable, 10-year, 15-year, 20-year, 25-year, 30-year). The insurance is designed to provide protection against “temporary financial risks”, such as covering a mortgage, funding college education needs for young children, replacing lost income in support of a household that have young children and any other financial risk that lasts for a limited period of time. As the coverage is finite, the cost of insurance is relatively low. Many term policies come are sold with “convertibility features”, which allow all or part of a term policy to be converted into a permanent policy at any time during the term period without the need for additional medical underwriting.

A permanent policy is life insurance that is conceptually permanent in nature (as long as the premiums have been paid). This is coverage that can conceptually last all of the insured’s life. This coverage is typically ideal for those who have a perpetual need for coverage, as there is a school of thought that believes that while needs for insurance change over time, they never really go away. A parent who gets life insurance for the benefit of his/her children may want to keep coverage in place to help provide for grandchildren or leave a bequest to a charitable cause. There are three general forms of permanent life insurance: (1) whole life, (2) universal life, and (3) variable universal life.

Permanent life insurance also has a “built-in savings component” that allows for the accumulation of cash value to grow within the policy. Depending on the type of permanent policy, the growth of the aforementioned cash value is attributed to guaranteed interest rates and possible mutual life dividends (whole life), general interest rates (universal life), and the performance of mutual fund sub-accounts (variable universal life). Due to the perpetual nature of the coverage and the cash value growth component, the cost of permanent insurance is significantly higher than comparable term insurance.

Some proponents are in favor of permanent coverage because they desire to have “something to show for their money” in the event that time comes to pass and the insured doesn’t die. One can access the cash value (potentially tax-free pursuant to Internal Revenue Code Section 7702) for a myriad of purposes, which we will discuss later. Term insurance, while cheaper, is sometimes viewed as a “zero-sum game”, where insurance company takes all of your premiums if you outlive the term of the policy.

Now getting to the “perm vs. term” debate. “Buy term and invest the difference” is, excuse my french, pure BS. Why? Because no one actually does it. I mean, it sounds good in theory and the numbers look nice on a spreadsheet, but it is simply not done in reality. So, where does that leave my thoughts on the issue? I believe that most clients will benefit from a combination of term and permanent life insurance – owning term life insurance to cover temporary life insurance needs (i.e., covering a mortgage, providing protection for young children, etc.) and have some permanent coverage for “ever-changing needs”, or for alternative strategies (which I will discuss in a future post).

This will conclude Part 1 of our “Real” Life Insurance Discussion. Stay tuned for the discussion next week, where I will discuss the different ways life insurance can be used (and should not be used) as part of a comprehensive financial plan. Thanks again for bearing with me, and feel free to seek me out on Facebook or Twitter to provide comments or feedback. Thanks.

Disclaimer/Disclosure

As I am a licensed life, health, disability, and long-term care insurance agent, I want to once again reiterate that the views that I express are mine alone – not that of any firm that I am affiliated with. In addition, my commentary is for information-sharing purposes only, and should not be considered financial, tax or legal advice. As always, any financial decision should be made with adequate information and, if possible and desired, the assistance of a licensed, competent and professional advisor that is unbiased and holds your financial interests above his or her own.

Hi there everyone.

I have been going through changes. Since my last post, I experienced the loss of my father, prayed as my mother dealt with a bout of pneumonia that would not go away, and finally, experienced the loss of a dear aunt who in all respects was the glue that kept my maternal family connected over the last 40+ years. I have spent the time dealing with a roller coaster of emotions and, in full circle fashion, I find myself back here to get back into discussion mode. I am very sorry about the hiatus and hope that we can pick up on things. The experiences in question have given me many topics that I want to discuss in upcoming posts.

Now, let’s talk about today’s topic – College, the financial impacts of the decisions being made, and why we need to rethink the way we approach it.

College – A Voyage to Higher Learning or A Rite of Passage?

As the end of the summer months are past us and the fall is underway, many families have completed an annual rite of passage otherwise known as college move-in. It is a time of pride, satisfaction, appreciation, and anxiety for what lies ahead – college. In 2017, 64.5% of US high school graduates matriculated to college, slightly lower from a high of 70.1% in 2009. As the statistics suggest, college is now identified by many families as the main pathway to a professional career across the US labor market. For many families, it is believed that in order to get a good paying job, you have to go to and graduate from college.

Being a college graduate myself, I totally agree with this sentiment. However, time and my experience as a financial advisor has taught me many things about the journey into higher education – (1) it can be an expensive trip (college tuition and fees have increased by 63% between January 2006 and July 2016; college textbook prices increased by 88% and room and board expenses increased by 51%), (2) bad choices can have effects that will haunt you and your kids for years to come (imagine paying student loans for a class that you dropped 10 years ago), and the toughest pill to swallow, (3) college is not for everyone.

With that said, I feel that a post is warranted to have a frank discussion about higher education and the mindset parents need to have when it comes to making smart, educated choices concerning one of the largest investments of your (or your child’s/dependent’s) life.

Let Me Tell You a Story

To illustrate part of the issue, let me start off things with a story. To protect privacy, I will not reveal the client’s name or sex, the client’s child’s name or sex, or the educational institutions involved. The only thing that I will reveal is that the schools in question are located in New Jersey.

In April of this year, while returning a tax return and records to a client, the client appeared distraught and withdrawn.

“What’s wrong?” I asked, sensing the client’s distress.

“[Child] didn’t get into [School A].”

“So sorry to hear.” was my reply, as I tried my best to be sympathetic. “How did [child] fare with the other choices?”

“Well, [child] got into [College B], but [child] would have to do a summer program out of pocket just to be able to take regular college courses in the Fall.”

Note: College A is a public university with an estimated annual cost (in-state tuition with room and board) of $26,000. College B is a private university with an estimated annual cost of $58,000. Both colleges are lower tier nationally ranked (i.e., ranked 100+) and comparable in college rankings with no distinguishable difference in the quality of education.

As the client is a tax client and not a financial planning/investment advisory client, I could only do my best console the client with encouraging words like “Congrats on the acceptance.” and “I’m sure that once the acceptances come in, you guys will make the best decision.” However, the advisor and financial counselor in me would have another conversation, and it would touch on the following topics:

A Different Take on Higher Education

In looking at the scenario I presented, along with other issues that I think are pertinent, here are the areas that I want parents and students alike to consider as they make decisions with respect to College:

Choosing a college based emotion is not a good idea – I see it too often. Parents and their children making a choice in college based on pride – focusing more on the name, the perceived prestige of the school, and the “experience” that the young adult will have vs. the education that he or she will receive. And colleges are in on the masquerade as well, by spending inordinate amounts of money on amenities rather than on strengthening curriculums with tenured professors, etc. Remember that college is not “young adult sleepaway camp.” It is the place that you are investing money to prepare your child for the professional lives that they will embark upon. The key words are “investment” and “education” here. While making friends and being in an environment where your child will feel comfortable and thrive are important, the ability to develop core 21st-century workplace skills like public speaking, collaboration, growth mindset, and teamwork is much more critical for long-term success post-college. Keep your eye on the ball.

Be careful with name brands – Did your child get into Georgetown and MIT? Which school would you choose? All logic would point to MIT given its name and eminence. What about getting into Georgetown and Brown? Brown is an Ivy League school, so would you choose Brown, right? Not necessarily. Studies show that students that get accepted to top schools like Harvard and MIT, but for one reason or another don’t attend (i.e., go to Georgetown or Emory instead), have had similar career success/outcomes relative to those that did go. So, rejoice that your child got into a top-tier school, but take a hard look at academics, costs, college quality of life, and career prospects when making your ultimate school choice.

There’s nothing wrong with Community College – In the past, I’ve heard jokes about community college. Chris Rock’s joke that community college “was like a disco with books” come to mind (“Here’s ten dollars. Let me get my learn on.”). All jokes aside, with the mounting costs of college and with a cohort of graduating students unsure of what they want to do and whether they will succeed in college right out of high school, enrolling in community college is a relatively inexpensive and prudent way to stick your toe into the deep end of the college/university pool.

It’s not how you start, it’s how you finish – To add to the value of community college, if a student does well and desires to continue on, most state colleges and universities guarantee acceptance of a quality student (GPA of 3.0 or better) and the credits they earned while in community college. Imagine getting a Rutgers University degree for nearly half the cost by doing two years in community college, doing well and transferring over. This is also an ideal approach for families who don’t have the funds for college and prefer to not take loans. Students can work and take classes, earn credits on their schedule and as they progress, matriculate to a 4-year college and make it work financially.

All kids are not built for college, and that’s ok – In his controversial book, Real Education, Charles Murray has argued that 50% of the students currently in college don’t belong there. His rationale is based on the historical population that colleges once housed – 20% of graduating seniors nationwide. The other cohorts historically went to professional school, apprenticeships in certain vocations, factory jobs or marriage and homemaking for young, newly wedded women. Obviously, those days are gone, and the US economy has moved from a manufacturing one to a service-based one. However, as Murray argues, archaic school systems have been incomparable in educational development, leading the production of graduates that are not ready for the rigors of college ( see the attached article). As there are no places for these graduates to go in this economy, colleges have stepped up to take them in. By admitting students who require more remedial courses before even engaging in college-level courses (more than 50% nationwide), it is argued that these students water down the rigor of college curriculum for those that do belong there (the aforementioned original 20%), and the nation’s education system suffers for it.

What is also lost is that students that otherwise would make excellent mechanics, plumbers, electricians, and construction workers miss the opportunity to develop in this vocation, while current professionals age without competent successors. In evaluating “no college required” vocations as an option after college, have a heart-to-heart conversation with your children. See what their passions are. Many careers can be realized without college (or very little of it). Exploring such opportunities while taking a community college course or two can be one way to test the waters on such vocations. The key is to not close your mind to the opportunity.

Important Financial Planning for Families with College-Age Children

Please make sure that you take note of the following financial planning tips when considering college with your young adult children:

Well, that’s all I have to share for now. Thank you so much for allowing me to share my post with you. Please feel free to reach out with questions or suggestions for new topis that you would like more information on in the future.

SAM

Happy New Year! I know that I have been busy, but I do come bearing gifts (of wisdom).

Graduating from college is a big deal. Not just for the education obtained, but for the commitment of focusing oneself for 4-5 years on a goal. All of those years of taking courses, managing your time, balancing assignments of varying priority, dealing with emergencies, and making it to the finish line. It’s definitely more than an academic endeavor. College in many ways shows prospective employers that you are ready to take on the rigors and responsibility that come with real work in the real world.

In my contemplation of graduates, I thought that it would be cool to share a few financial words of wisdom as they prepare to venture out into the real world. Here are my ten pointers for young professionals coming out of college:

1. Save 25-35% of your net pay. You never had the money before, so you will never miss it. Start building your war chest of savings now, because it will come in handy later.

2. If you have student loans, use every disposable dime (after saving per #1) to pay it off. I’m serious. Get rid of those loans.

3. INVEST money in 1-2 custom-made suits, custom-made shirts, some high-quality shoes, and a nice coat. It will cost some serious money, but if you are on the lookout for deals (i.e., finding a quality tailor, looking out for yearly deals from stores like NORDSTROM, tagging along to a friends and family event at a luxury retailer, etc.), you will be amazed by the money that you can save. There will be times when you need to look like you have a million bucks. Be ready.

4. Start developing a Secondary source of income. Start off with a Stock Dividend Fund, a Municipal Bond or Treasuries. Then, consider investing in an investment or rental property. Invest in a business or restaurant. Whatever. The point is, you will do yourself a favor by growing a source of income that is NOT from your job. Don’t be a slave to a paycheck.

5. Sign Up for Match – As in your 401(k) Match. Since your income is expected to be relatively low, here’s a retirement savings trick that I would recommend – Contribute to your 401(k)/Roth 401(k) just enough to secure the company’s match (which is free money), stop contributing after that and max out a ROTH IRA. Many employer Retirement Savings Plans have mediocre investment options at best and are full of hidden fees. Having a Roth IRA allows you to build assets that you can control with many cost-effective, high performing investment options.

6. CASH rules EVERYTHING around me (CREAM). If you can’t pay for it with cash (and I’m not referring to your savings), don’t buy it. Credit is not an extension of your income. It is BORROWED MONEY. Nothing is sadder than seeing a young adult paying on a credit card balance for clothes that he/she bought a year ago, or for a trip that you took two summers ago. Learn to live your life and pay your bills with cash. You will thank me for it later.

7. Be Pennywise… and I don’t mean that big-headed clown from It. Live frugally. Notice that I did not say “cheap”. Being frugal is all about being an informed and vigilant consumer. You take the time to shop for the best deal possible, You take the time to research alternatives and options (rummage sales, goodwill stores, etc.). You make informed decisions. You set limits for how much you will spend and you try your best to stay within those limits. You budget and save for big purchases and you set aside funds for splurging. You understand who you are, what your attitude is about money and try to protect yourself from yourself. It takes practice, but you will be thankful that you did this now vs. later.

8. Understand that all things that glitter, isn’t gold. You will have friends that have a new car, bought those $100+ jeans, partied last weekend in VIP at ‘the club’. They’re living this fabulous lifestyle. However, they have no assets, bank account is just above the minimum (if not constantly incurring overdraft fees), and they’re barely making ends meet. This is not a judgement – just an observation. When you’re young, its natural to want to go out and have fun, but you have to be smart. If you need a car, buy a used one with cash (you will be amazed by what you can get for $5-10k). Budget for that fun and don’t get carried away. Leave charge cards at home and pay with cash. If you plan to do it up big, plan for it a month or two in advance and work it into your budget (Note: that you will have to cut back somewhere, so be prepared to paper bag your lunch for a few weeks). The point is, everything has a cost, so be considerate of what frivolous spending can have on your long-term goals.

9. Luxurious Living costs you big time. Thinking about moving to the “hot urban areas” with the brand new apartment complexes? With one bedrooms costing nearly $2,000/month ($24,000/year), you say “what the heck… you only live once, right?” That may be true, but if you were able to find a studio a few miles away at $1.250/mo ($15,000/year), you can save $9,000 year which could go towards, savings, investments or retirement. That same $9,000 saved in that one year could grow to $235,197 in 40 years towards your retirement (assumed the 30-yr return of the S&P 500 of 8.5%).

10. Speak to a professional. You may not necessarily be ready to work with a financial advisor year-round, but it doesn’t hurt to pay a few hundred dollars to meet with an accountant and a fee-only advisor to discuss tax, budgeting and investment strategies for the ensuing 6-12 months. Also, you can utilize tools like Mint.com , Betterment.com, Learnvest.com, if you feel comfortable and savvy enough to navigate through this with a little help.

Well, I hope that this information is useful to you. Please provide me with feedback via twitter. I would love to hear from you. Thanks and watch those pennies!

Hello once again! I am so sorry for the brief hiatus. Things get so busy from time to time and I am terrible at putting activities into daily slots. However, I am committed to this endeavor and will have to dedicate time to writing in order to make sure that I am bringing relevant and interesting content to you on a regular basis. My goal is to get out a minimum of two posts per week. I hope to get on this regular scheduling starting next week. Thanks so much for your understanding.

Now on to today’s topic ….. How do you pick stocks?

Memorable Quotes About Stocks

These quotes say a lot more about investing in stocks than most of what this post will, but if you can humor me for a few moments, I will add more color to some of these timeless quotes on the art of stock picking.

Are you an investor, trader or speculator?

So, the first question I will typically ask a client is whether they are an investor, trader or speculator.

Note – Before I dive into this, please be aware that I am “going light” on this topic. I am not going to get into Top-Down Analysis, Bottom-Up Analysis, Charting, or hard core fundamental analysis (e.g., Discounted Cash Flow Analysis), etc. At least not yet. So bear with me as I break it down for common folks without MBAs in Finance (smile).

So, what’s an investor? To keep things simple, we will define investors as individuals that are interested in buying stable, well-run companies and do not have a defined date for selling the stock (as long as the company continues to run well and its stock price is relatively stable). So hypothetically, these can be purchases that can be made, and the stock held indefinitely. This post is mainly for investors.

Traders are individuals that buy in and out of stocks. They can hold stocks for months, weeks, days, hours, minutes, and even seconds! Traders look for large swings in the price of a stock to make profits. Another distinction for traders is that they don’t necessarily buy a stock with the hope that the stock will go up in value. Short sellers or put option buyers trade with the hope that a stock will decline in value. “Short” activity on a stock can sometimes act as a leading indicator as to whether a stock will change in value – not necessarily due to fundamental flaws in the stock’s business, but due to market/trading forces (i.e., a stock can go up in value simply because short sellers have to “cover” their shorts by buying shares). I will get into puts and shorts on another post, but just understand that traders typically take short-term positions on a stock that can be based on a positive (hope that the stock will go up) or a negative (hope that the stock will go down) bias. This post is not for traders, so if you’re looking to trade stocks, this post isn’t for you.

Speculators are simply people who buy heavily depreciated stocks or short highly priced stocks in hopes of making a profit. They take positions that can be either short-term or long-term in nature. Again, this is a post for investors, so I am not going to get into speculation at this time.

Identifying Stocks for Investors

Here are some thoughts/ideas and pointers for identifying stocks that might appeal to you as an investor:

You read it right, she made more than 15% in three months. That’s over $1,500 made on a $10,000 investment made in 90 days. Compare that to the less than 1% that you can get from a checking account, or 1.85% for an 18-month CD. Look at companies behind the goods and services you buy every day. Go online and do some research. Are these companies profitable? Do their profits and/or performance have a track record of going up consistently? Are they among the top 5 participants in their respective industries? Is the stock price steady growing? Does the stock pay nice dividends? If there are enough “yes” answers to these questions, you may have a stock that you can invest in.

Conclusion (for now)

There is no foolproof way for picking winning stocks, so understand that it is likely that when investing in individual stocks you will pick winners and losers. If you have the stomach to get through it and learn from the experience, I do encourage you to embrace this wealth building activity. Lastly, you should consider building the foundation of your portfolio with broad-based market exposure via a low-priced stock market index fund or ETF. Then you can look to invest in single name stocks to help enhance growth opportunities.

I hope that you found this post informative and helpful. As always, I am available if you have questions to discuss. In the meantime, good luck!